[ad_1]

It’s an end of an era.

That’s BlackRocks Inc.’s

BLK,

Tony DeSpirito, chief investment officer in the U.S. fundamental equities division of the world’s largest asset manager, telling investors to prepare for the end of a backdrop of low-rates and slow-growth that’s defined markets since the 2008 global financial crisis.

Despite a precarious start to 2022, “one thing we feel relatively certain about is that we are exiting the investing regime that had reigned since the Global Financial Crisis (GFC) of 2008,” DeSpirito wrote in a second-quarter outlook Monday.

The equities group sees not only a “new world order” taking shape that will “undoubtedly entail higher inflation and rates than we knew from 2008 to 2020,” but a trickier environment for investors, particularly as Russia’s war in Ukraine threatens to keep energy

CL00,

and commodity costs in focus.

“Perversely, the situation could favor U.S. stocks, as they are more insulated than their European counterparts from energy price spikes and the direct impacts of the war and its economic ramifications,” DeSpirito wrote, adding that a rebalance toward value may be warranted.

“It is also worth noting that bonds, which typically gain an edge in times of risk aversion, are providing less portfolio ballast today as correlations to equities have converged.”

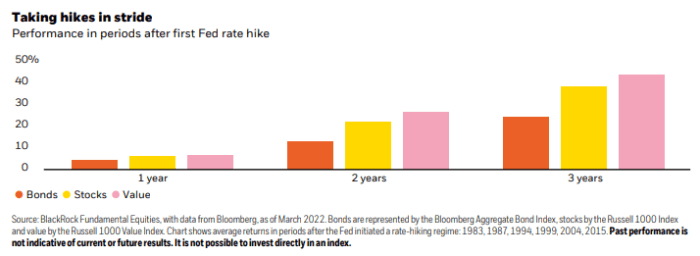

To help form its thinking, the team studied previous rate-hiking cycles by the U.S. central bank, starting in 1983 to 2015, and found that value stocks outperformed their large-capitalization counterparts but also a key bond-market benchmark (see chart).

Stocks, bonds and especially value tend to do well 3 years after a rate-hiking cycle

BlackRock Fundamental Equities, Bloomberg

The team compared the performance for the Bloomberg U.S. Aggregate Bond Index (red), the Russell 1000 index

RUI,

(yellow) and the Russell 1000 Value Index

RLV,

(pink). Of note, performance was positive across all three segments, in the first three years after rates started to increase.

Other assumptions of the outlook were for inflation to recede from 40-year highs later this year, with the cost of living to settle above the 2% level typical before the pandemic, perhaps in a 3% to 4% range, in a worst-case scenario.

The team also expects the 10-year Treasury yield

TMUBMUSD10Y,

to push higher as the Federal Reserve looks to raise its key rate, but that it “would need to reach 3% to 3.5% before we would question the risk/reward for equities.”

The benchmark Treasury rate, which neared 2.4% on Monday, is used to price everything from corporate bonds to commercial property loans. Higher Treasury rates can translate to tougher borrowing conditions for big companies at a time when inflation pressures also can pinch margins.

Still, DeSpirito sees potential for an “underappreciated opportunity in companies” with a record of passing higher costs on to consumers, even if they now face inflation pressures.

“The period of extremely low interest rates was very good for growth stocks —and very challenging for value investors,” he wrote. “The road ahead is likely to be different, restoring some of the appeal of a value strategy.”

Stocks rallied on Monday, led by the technology-heavy Nasdaq Composite Index

COMP,

as it recorded its best day in more than a week, with the S&P 500 index

SPX,

and Dow Jones Industrial Average

DJIA,

also booking gains.

Source link